Finance is one of the few industries where AI models being successfully implemented is nowhere near enough.

Institutions have to explain why it worked, whether customers were treated fairly, whether records were retained properly, and whether regulators could reconstruct the process later if needed.

That is where compliance-friendly AI content enters the conversation.

Once AI starts touching lending decisions, financial promotions, fraud reviews, customer servicing, or compliance operations, the standard changes immediately.

The Edelman Trust Barometer continues showing how fragile public confidence becomes when organizations mishandle technology, transparency, or personal data.

The conversation stops being about efficiency alone and starts becoming about defensibility.

Understanding Compliance in Finance

On paper, compliance sounds straightforward: follow the rules that protect consumers and maintain fair markets.

In practice, financial compliance is a layered system of overlapping obligations, documentation requirements, review processes, and regulatory interpretations that rarely stay static for long.

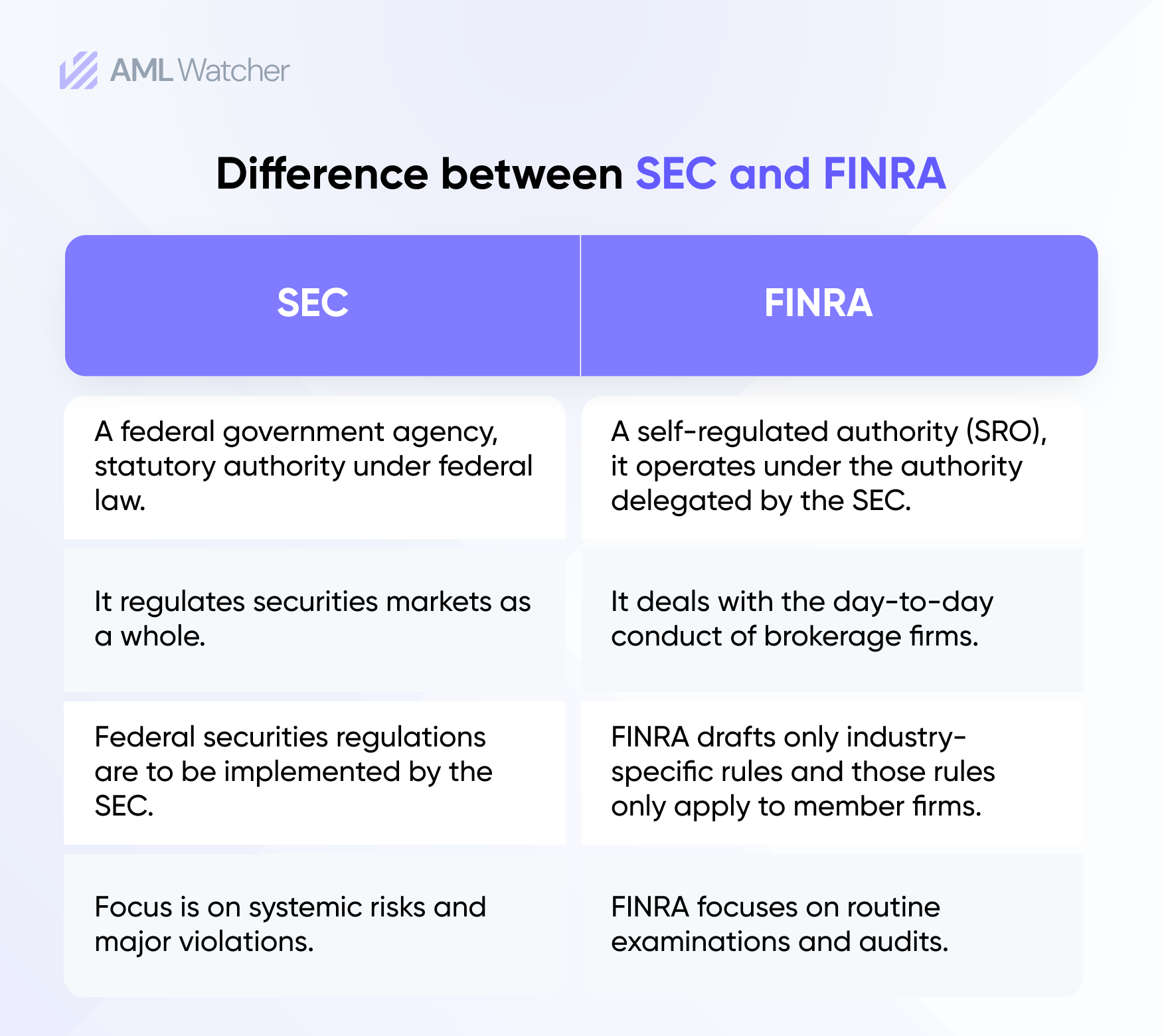

Firms operating in the U.S. deal with regulators like the U.S. Securities and Exchange Commission (SEC) and FINRA.

UK institutions answer to the Financial Conduct Authority (FCA). Global organizations also navigate privacy frameworks like the EU’s General Data Protection Regulation (GDPR).

The operational implications show up everywhere:

- Marketing communications have to remain fair, balanced, and non-misleading under rules like FINRA 2210.

- Lending decisions have to comply with the Equal Credit Opportunity Act.

- Customer data handling must align with frameworks such as the Gramm-Leach-Bliley Act.

And those requirements do not disappear because an AI system generated the output instead of a human employee.

Teams assume the risk sits inside the model itself. Most of the time, the real exposure appears in the workflow surrounding the model:

- Who reviewed the output

- What policies governed generation

- Whether decisions were documented

- Whether disclosures stayed intact

- Whether exceptions were escalated correctly

- Whether someone can explain the reasoning six months later during an audit or dispute

A system can technically perform well and still become unusable inside a regulated environment if nobody can clearly explain how decisions were made.

The Role of AI in Financial Services

AI now touches a surprising amount of day-to-day financial infrastructure.

Fraud detection is one of the clearest examples:

- Machine learning systems process enormous transaction volumes in real time and identify suspicious patterns far faster than manual review teams could realistically manage alone.

- Underwriting models evaluate predicted default risk and surface contributing variables behind decisions.

- Customer support systems generate responses that follow internal policy language and approved communication standards.

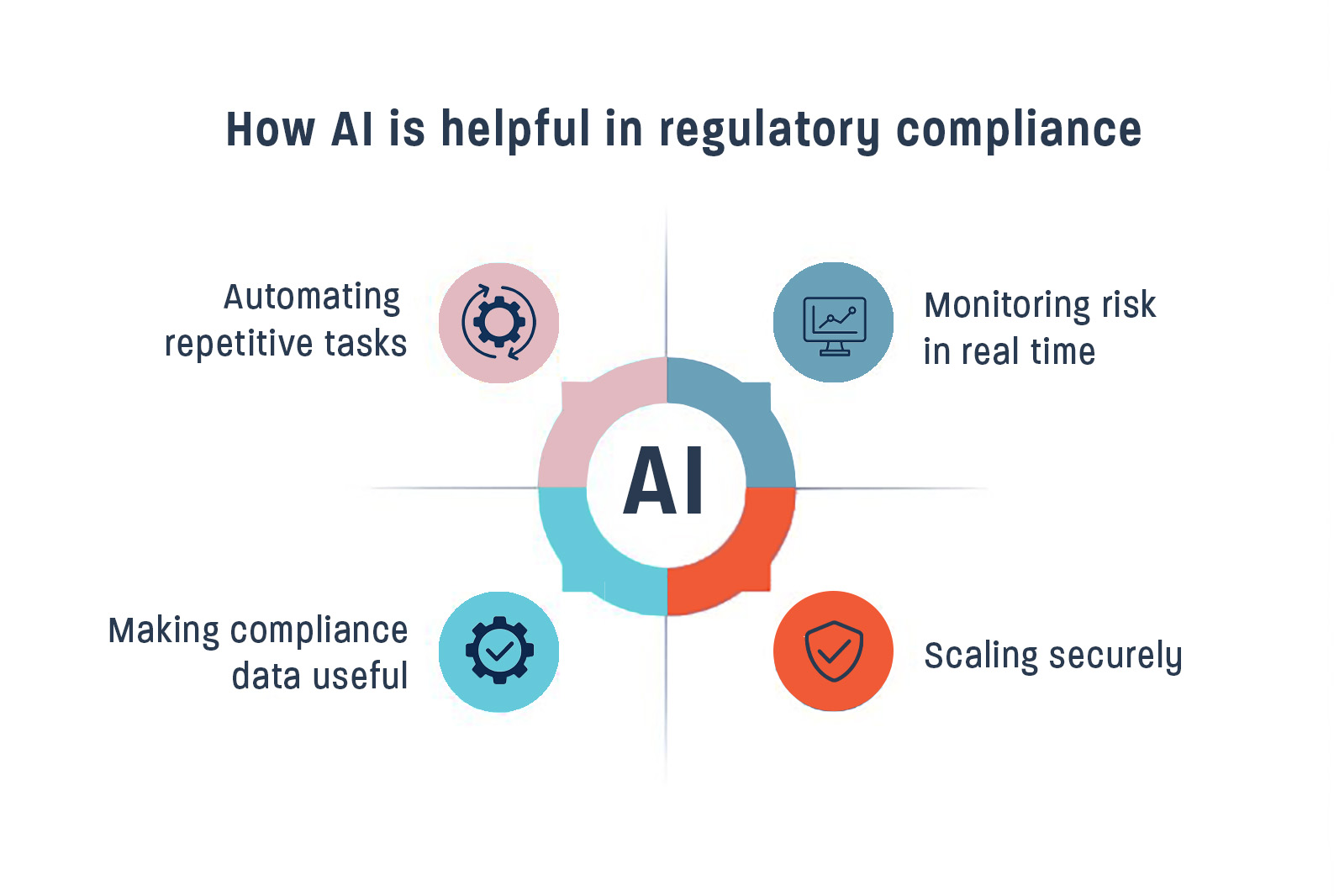

- AML teams use AI to reduce the operational burden created by escalating alert volumes.

AI can do these tasks at scale, which changes the scrutiny level.

Research from the Bank of England and FCA found that machine learning adoption has moved steadily from experimentation into production use across financial services, particularly in risk management and compliance functions.

The Financial Stability Board has also documented AI’s growing role in improving operational efficiency and decision-making across the sector.

What gets lost in a lot of AI discussions is how operational these deployments actually are.

Most banks are not replacing entire departments with autonomous systems, but trying to reduce friction inside existing processes:

- Fewer false positives

- Faster review cycles

- More consistent documentation

- Lower manual workload

- Faster escalation routing

- Quicker customer response times

Very unglamorous problems.

But those are usually the problems that matter most inside large financial organizations.

Challenges of Compliance in AI-Driven Finance

This is where things get complicated.

AI introduces speed and scale, but it also introduces new failure points that traditional governance structures were not designed to handle.

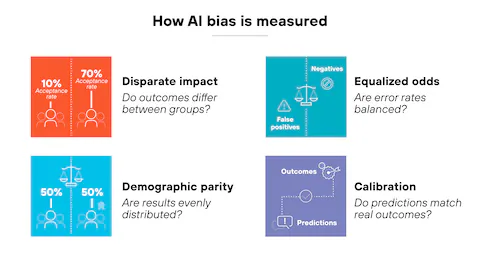

Bias remains one of the biggest concerns. Here’s how:

- If training data reflects historical discrimination or skewed decision patterns, models can reinforce those outcomes at scale.

- Black-box systems create additional problems because institutions may struggle to explain why certain lending or fraud decisions occurred.

- Large language models add another layer of risk entirely: confidently written outputs that are partially inaccurate, outdated, or unsupported.

Jeffrey Zhou, CEO and Founder of Fig Loans, works in consumer lending, where explainability requirements become operational very quickly once automated systems start influencing customer outcomes.

He explains, “In lending, customers are directly affected by how these systems behave, so explainability cannot be treated as optional. If a model shifts, approval patterns shift. If monitoring weakens, fairness issues become harder to detect early. The operational challenge is making sure governance evolves alongside the systems instead of lagging behind them.”

And finance has very little tolerance for that type of ambiguity.

Especially once customer outcomes are involved.

Regulators have started responding accordingly:

- The EU AI Act introduces new expectations around transparency, risk classification, and oversight.

- In the U.S., guidance like the Federal Reserve’s SR 11-7 model risk management framework continues emphasizing governance, validation, documentation, and explainability for systems influencing decisions.

The operational reality is that many compliance teams are now trying to evaluate systems that evolve faster than their review structures were originally designed for.

That creates friction internally.

Say, engineering teams want deployment speed, while compliance teams want documentation. Product teams want usability. Leadership wants efficiency gains quickly enough to justify investment.

Those priorities do not naturally move at the same pace.

Gregor Emmian, Deputy Chief Digital Growth Officer at Rise, works in fintech growth environments where AI systems, operational workflows, and compliance oversight often need to evolve simultaneously.

“The difficult part is usually not deploying the system initially. It’s maintaining consistency once different teams start interacting with the workflows in different ways.” Emmian shares,

“Product wants iteration speed, compliance wants reviewability, legal wants tighter controls, and operations wants stability. If governance standards are unclear early, small inconsistencies compound very quickly.”

And when they become disconnected, institutions usually end up in one of two bad positions:

- AI deployment slows to a crawl because governance becomes reactive and overloaded

- Or systems move forward faster than oversight processes can realistically support

Neither scales well.

What Is Compliance-Friendly AI Content?

Compliance-friendly AI content is not simply AI-generated content with disclaimers attached afterward.

These systems are designed so governance exists inside the workflow itself rather than sitting outside it as a cleanup.

The distinction matters.

The stronger systems build controls upstream.

Jason Ledbetter works closely with businesses scaling operational systems across marketing, workflow, and customer-facing processes.

He notes, “The output itself is usually not where the long-term problems start. It’s the surrounding process, prompt changes nobody tracked, inconsistent approvals, unclear ownership between teams, or systems evolving faster than documentation standards around them.

Once that happens across multiple departments, fixing it retroactively becomes extremely difficult.”

That usually starts with a few foundational elements.

Transparency

Teams need visibility into how outputs were generated:

- What data sources influenced responses

- What assumptions existed

- Where limitations exist

- Whether external retrieval systems were used

- Which policies governed generation

Not every model needs perfect explainability. But if institutions cannot reasonably explain outcomes, regulators and internal governance teams eventually lose confidence in the process.

Accountability

Someone has to own decisions.

That sounds obvious until organizations deploy AI across multiple business units and nobody is entirely certain who reviews exceptions, who approves policy updates, or who signs off on edge-case outputs.

Strong governance structures define escalation paths early:

- What requires human review

- Which outputs are auto-approved

- When legal review becomes mandatory

- How incidents get documented

Without that clarity, operational confusion shows up very quickly.

Regulatory alignment

AI systems still need to comply with existing financial regulations around disclosures, claims, data handling, recordkeeping, and fairness obligations.

The important thing here is that regulators generally do not care whether the problematic output came from a human or a model.

The institution remains responsible either way.

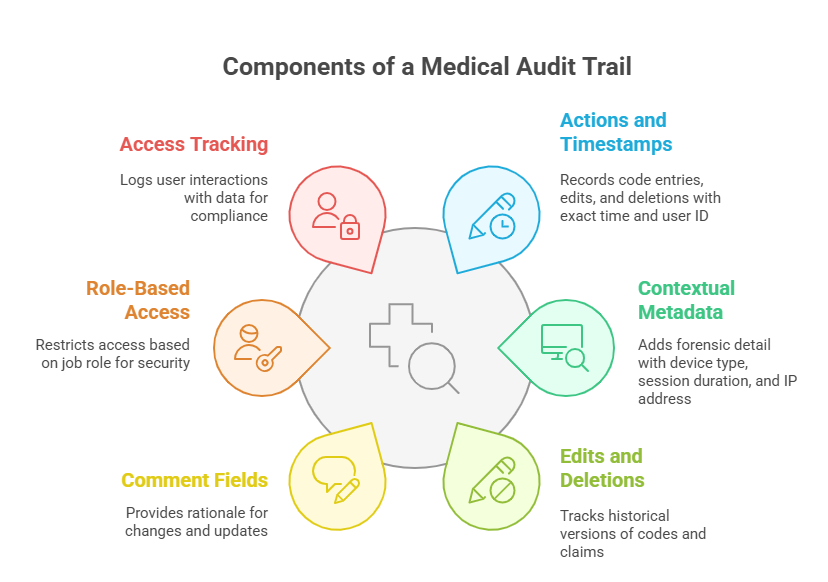

Auditability

This becomes critical once AI moves into customer-facing or decision-influencing workflows.

Institutions need version histories, prompt tracking, policy records, model documentation, and defensible audit trails that reconstruct how outputs were produced.

Because eventually somebody will need to trace it backward.

And reconstructing undocumented AI decisions after the fact is usually miserable work.

Guardrails

Guardrails are where many systems either stabilize or fall apart operationally.

Practical safeguards include:

- PII redaction

- disclosure enforcement

- retrieval restrictions

- policy-aware prompting

- prohibited claims filtering

- escalation triggers

- approval routing for higher-risk outputs

These controls are not glamorous. But they are often the difference between scalable deployment and constant remediation work afterward.

The NIST AI Risk Management Framework has become a practical reference point for many institutions seeking to formalize these governance processes.

The Future of Compliance-Friendly AI in Finance

The next phase of AI adoption in finance will probably depend less on raw model capability and more on explainability, governance maturity, and operational trust.

Samantha St Amour, Partnerships Manager at Technobark, says, “Financial institutions are moving past the question of whether AI can improve efficiency.

The bigger concern now is whether systems can remain explainable, auditable, and operationally stable once they scale across multiple departments. The organizations seeing long-term success are usually the ones building governance into the workflow early instead of trying to retrofit controls later.”

That shift is already happening.

A few years ago, most conversations focused on whether models could perform tasks accurately enough to justify adoption. Now institutions are asking harder questions:

- Can outputs be explained clearly

- Can decisions be reconstructed later

- Can governance scale alongside deployment

- Can systems survive regulatory scrutiny

- Can risk teams actually manage the operational complexity being introduced

Those questions matter more over time, not less.

The same pattern is appearing across other highly regulated industries as well.

Healthcare platforms handling sensitive patient workflows, prescription management, or areas like testosterone replacement therapy are facing many of the same pressures around explainability, documentation standards, privacy controls, and auditability as AI adoption increases.

Explainable AI is becoming increasingly important because firms need systems that surface reasoning in ways auditors, compliance officers, and regulators can realistically interpret.

That does not mean exposing every mathematical detail behind a model. But it does mean institutions need clearer visibility into how outcomes are produced and why certain decisions were reached.

Auditability will likely evolve alongside that.

Tamper-evident logging systems and blockchain-based verification models are already being explored as ways to strengthen recordkeeping and preserve decision histories more reliably over time.

Next Steps

Financial institutions exploring AI should focus less on maximum automation and more on operational control.

Tools can help, especially platforms built around policy-aware generation, version tracking, disclosure consistency, and audit support.

Writecream is one example of a platform working toward those practical guardrails through prompt templates, structured workflows, and logging capabilities designed to support reviewability.

{kind=link}

{kind=link}

{kind=link}